The current market environment has been defined by a significant downturn in global equities, prompting a widespread search for stability. Worries over the massive capital expenditure required for artificial intelligence (AI) have shaken investor confidence, with AI heavyweights like Nvidia (NVDA) falling over 8% for the past month and other giants like Oracle (ORCL) and Alphabet (GOOG) seeing significant drops on news related to AI spending and competition. This risk-off period, fuelled by jitters in the previously high-flying tech trade alongside persistent inflation, has brought the historical role of precious metals as a safe haven into sharp focus.

However, a closer look at the data from 2025 reveals a fascinating and crucial divergence: not all precious metals are performing equally.

This analysis explores the dynamics of the current market, examines why silver and platinum have outshone gold and takes a look at the powerful relationship between silver and its miners.

Why Silver and Platinum Took the Lead

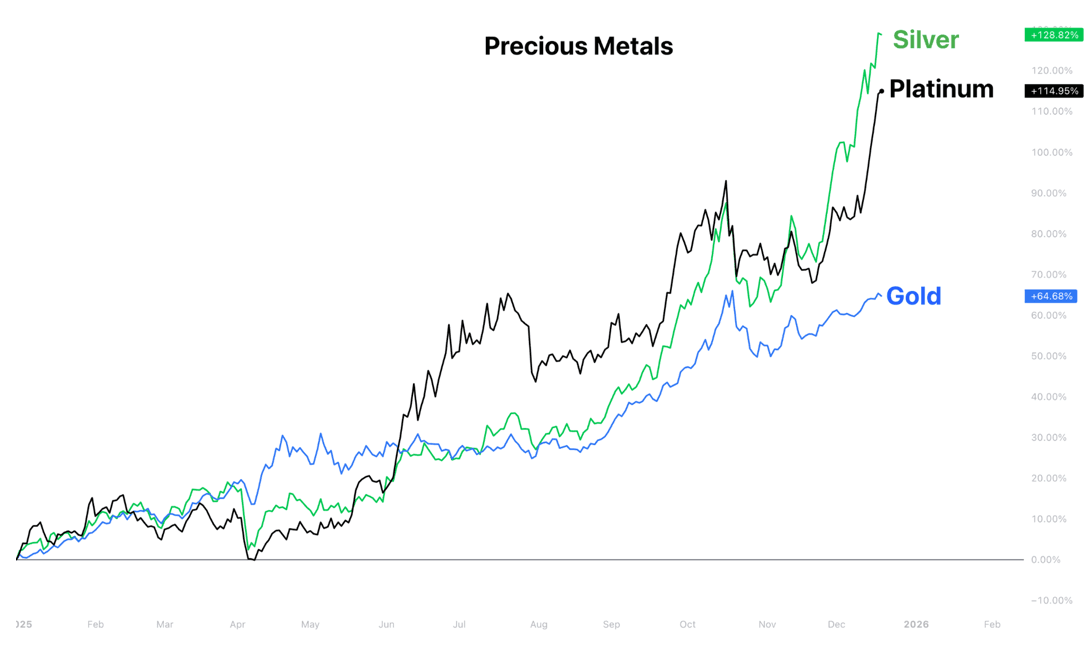

While gold is the traditional headline-grabber in times of crisis, 2025 has told a different story. As the chart below illustrates, silver and platinum have delivered significantly higher returns, challenging the long-held status of gold as the undisputed king of safe havens.

As of mid-December 2025, silver has returned approximately 120% and platinum 110%, both substantially outpacing gold’s respectable 60% gain.

This outperformance is rooted in the dual nature of these two metals:

In essence, while gold has performed its traditional role as a stable store of value, silver and platinum have benefited from a powerful combination of being both a safe haven and a play on the industrial and technological trends of the future.

Silver vs. Silver Miners

For those analysing the silver market, an even more compelling story emerges when comparing the metal itself to the companies that mine it. Silver mining stocks are often viewed as a leveraged play on the price of silver. This means their stock prices tend to move in the same direction as the metal but with greater magnitude, for two key reasons:

● Operational leverage: A mining company has fixed costs (labour, equipment, energy). Once the silver price exceeds these costs, every dollar increase in the price of silver can translate into a much larger percentage increase in the company’s profits.

● Market sentiment: Mining stocks attract significant speculative interest. When the price of silver is rising, traders and investors often pile into mining stocks in anticipation of future profit growth, amplifying the upward move.

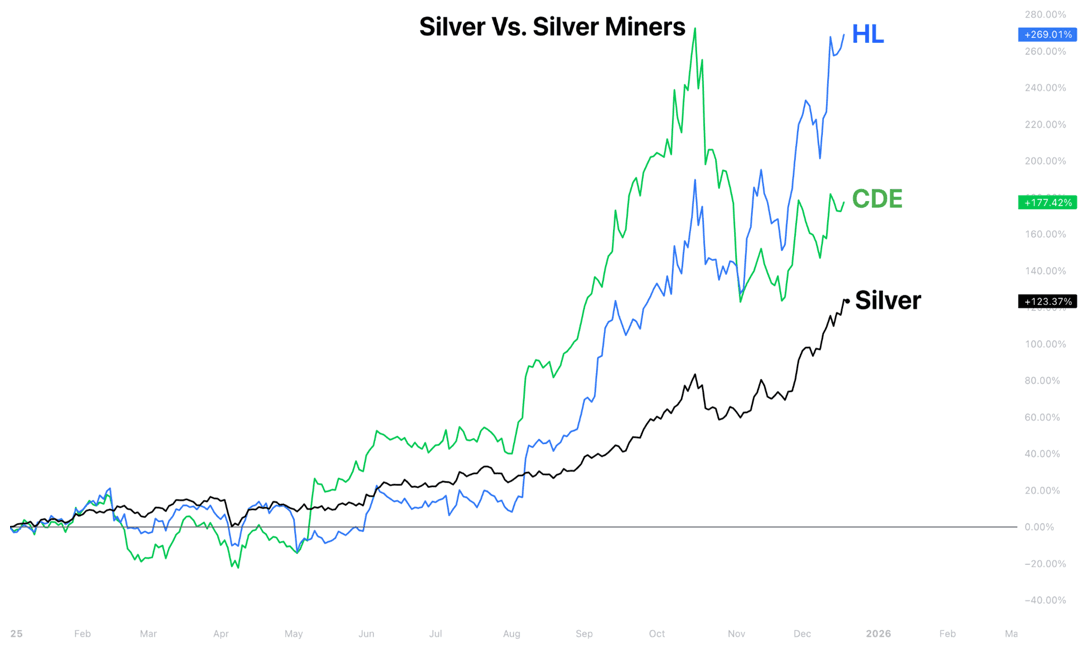

The chart below vividly illustrates this dynamic, comparing the performance of silver with two prominent US-listed silver miners, Hecla Mining (HL) and Coeur Mining (CDE).

The chart clearly shows the power of leverage. While silver delivered an impressive 120% return, Hecla Mining (HL) soared 290% and Coeur Mining (CDE) jumped 200%.

● Hecla Mining (HL): As the largest primary silver producer in the United States, Hecla’s identity is fundamentally tied to silver. The company’s strength lies in its high-grade, long-life assets, particularly the Greens Creek mine in Alaska, which is one of the largest and lowest-cost silver mines globally. With proven and probable silver reserves totalling over 200 million ounces, Hecla has a multi-decade pipeline of production. This huge reserve base means the company is well-positioned to capitalise on sustained higher silver prices for years to come, making it a cornerstone for many long-term silver investors.

● Coeur Mining (CDE): Coeur Mining offers a blend of silver and gold production, with significant operations across North America. Its key asset for silver exposure is the Rochester mine in Nevada, which recently underwent a major expansion designed to increase production and extend its mine life well into the next decade. Coeur’s strategy has been focused on investing heavily in exploration and development to grow its reserve base, which now stands at over 300 million ounces of silver and several million ounces of gold. This focus on growth means Coeur is not just a play on the current silver price but also on its ability to expand future production, offering a different but equally compelling long-term investment thesis.

Platinum vs. Platinum Miners

For those analysing the platinum market, an even more compelling story emerges when comparing the metal itself to the companies that mine it. This is especially true given that the platinum industry is one of the most geographically concentrated in the world. South Africa holds over 90% of the world’s known platinum reserves, making the companies listed on the JSE undisputed global leaders of the sector.

Platinum mining shares are often viewed as a leveraged play on the price of platinum. This means their stock prices tend to move in the same direction as the metal but with greater magnitude because the market is concentrated in South Africa. Global events, currency fluctuations, specifically the USD/ZAR exchange rate, and investor sentiment toward the region can significantly amplify movements in these shares.

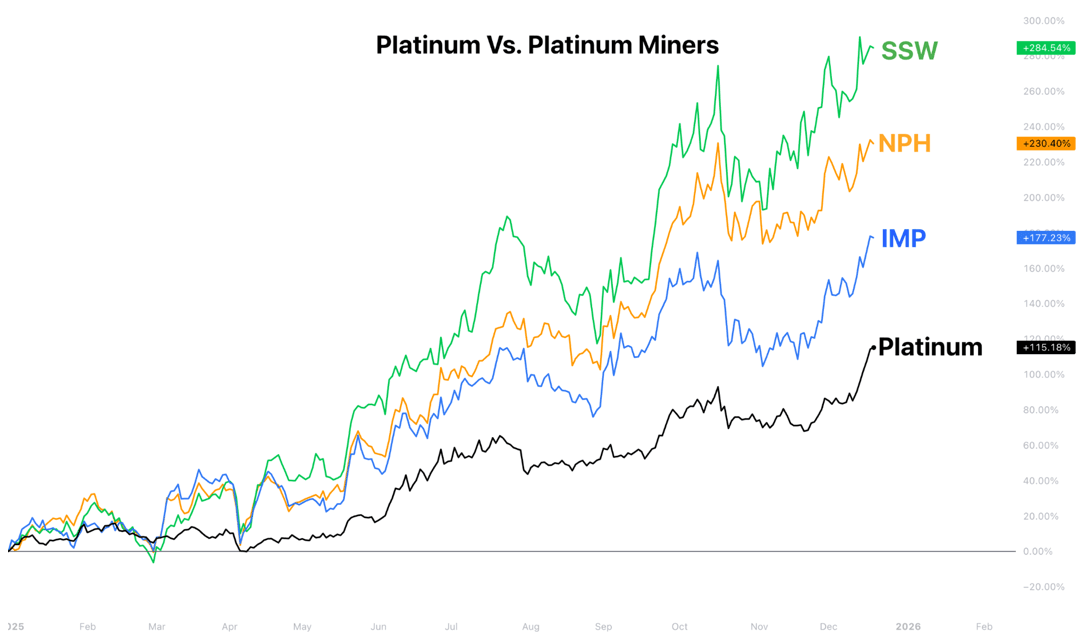

The chart below illustrates this dynamic, comparing the performance of platinum with several of these prominent South African miners.

The chart clearly shows the power of leverage. While platinum delivered an impressive 110% return, its leading miners soared even higher. Sibanye-Stillwater (SSW) surged 280%, Northam Platinum (NPH) jumped 230%, and Impala Platinum (IMP) gained 170%.

● Sibanye-Stillwater (SSW): A true global precious metals powerhouse, Sibanye-Stillwater is a producer from South Africa’s Bushveld Complex, the world’s richest PGM deposit. It uniquely pairs this with its ownership of the only primary PGM mines in the U.S., giving it unparalleled geographical diversification. With a massive reserve base across both continents, the company’s profitability is directly and powerfully linked to the prices of platinum and its sister metals, making it a go-to for investors seeking large-scale, diversified exposure.

● Impala Platinum (IMP): As one of the world’s most significant and integrated PGM producers, Impala’s operations are centred on the Bushveld Complex, where it runs some of the largest platinum mines on earth. Its scale is a major strategic advantage, allowing it to process millions of ounces of PGMs annually. With reserves that ensure decades of future production from this unique geological formation, Impala’s performance is a direct reflection of the health of the PGM market, offering investors a strong, large-cap way to gain exposure.

● Northam Platinum (NPH): Northam has established itself as a producer of high-quality, high-grade PGMs exclusively from its assets within the Bushveld Complex. The company has pursued an aggressive growth strategy, acquiring assets to build a long-life production profile from this world-class resource. As a more “pure-play” PGM producer focused solely on this region, Northam’s stock is exceptionally sensitive to platinum price changes, offering a potent investment thesis for those with a bullish outlook on the metal itself.

A Framework for Your Decision

So, what should an investor do in a market downturn? The analysis of 2025 reveals clear divergences; industrial metals like silver and platinum are outperforming gold, and mining equities are offering leveraged returns on the metals themselves.

This presents several strategic pathways for consideration:

● The defensive path: One could analyse the stability of assets with strong industrial demand, like silver and platinum, as a potential counterbalance to equity market volatility.

● The value path: Another approach is to view the downturn as an opportunity, researching whether high-quality mining companies with vast reserves now represent a discounted value.

● The momentum path: A third strategy involves focusing on relative strength, exploring why certain assets (the miners) are outperforming others (the metals) and what that might signal for future performance.

The question is not if there is an opportunity in this market, but which of these opportunities best fits your investment thesis.

Disclaimer:

*Any opinions, views, analysis, or other information provided in this article is provided by BROKSTOCK SA trading as BROKSTOCK as general market commentary and should not be viewed as advice according to the FAIS Act of 2002. BROKSTOCK SA does not warrant the correctness, accuracy, timeliness, reliability, or completeness of any information provided by third parties. You must rely upon your judgement in all aspects of your investment decisions, and all decisions are made at your own risk. BROKSTOCK SA and any of its employees shall not be responsible for and will not accept any liability for any direct or indirect loss, including, without limitation, any loss of profit which may arise directly or indirectly from the use of the market commentary. The content contained within the article is subject to change at any time without notice. BROKSTOCK SA is an authorised financial services provider - FSP No. 51404. T&Cs and Disclaimers are applicable: https://brokstock.co.za/

** This article was prepared by BROKSTOCK analyst Maboko Seabi

© 2025 BROKSTOCK SA (PTY) LTD.

BROKSTOCK SA (PTY) LTD is an authorised Financial Service Provider and is regulated by the South African Financial Sector Conduct Authority (FSP No.51404). BROKSTOCK SA (PTY) LTD Proprietary Limited trading as BROKSTOCK. BROKSTOCK SA (PTY) LTD t/a BROKSTOCK acts solely as an intermediary in terms of the FAIS Act, rendering only an intermediary service (i.e., no market making is conducted by BROKSTOCK SA (PTY) LTD t/a BROKSTOCK) in relation to derivative products (CFDs) offered by the liquidity providers. Therefore, BROKSTOCK SA (PTY) LTD t/a BROKSTOCK does not act as the principal or the counterparty to any of its transactions.

The materials on this website (the “Site”) are intended for informational purposes only. Use of and access to the Site and the information, materials, services, and other content available on or through the Site (“Content”) are subject to the laws of South Africa.

Risk notice Margin trading in financial instruments carries a high level of risk, and may not be suitable for all users. It is essential to understand that investing in financial instruments requires extensive knowledge and significant experience in the investment field, as well as an understanding of the nature and complexity of financial instruments, and the ability to determine the volume of investment and assess the associated risks. BROKSTOCK SA (PTY) LTD pays attention to the fact that quotes, charts and conversion rates, prices, analytic indicators and other data presented on this website may not correspond to quotes on trading platforms and are not necessarily real-time nor accurate. The delay of the data in relation to real-time is equal to 15 minutes but is not limited. This indicates that prices may differ from actual prices in the relevant market, and are not suitable for trading purposes. Before deciding to trade the products offered by BROKSTOCK SA (PTY) LTD, a user should carefully consider his objectives, financial position, needs and level of experience. The Content is for informational purposes only and it should not construe any such information or other material as legal, tax, investment, financial, or other advice. BROKSTOCK SA (PTY) LTD will not accept any liability for loss or damage as a result of reliance on the information contained within this Site including data, quotes, conversion rates, etc.

Third party content BROKSTOCK SA (PTY) LTD may provide materials produced by third parties or links to other websites. Such materials and websites are provided by third parties and are not under BROKSTOCK SA (PTY) LTD's direct control. In exchange for using the Site, the user agrees not to hold BROKSTOCK SA (PTY) LTD, its affiliates or any third party service provider liable for any possible claim for damages arising from any decision user makes based on information or other Content made available to the user through the Site.

Limitation of liability The user’s exclusive remedy for dissatisfaction with the Site and Content is to discontinue using the Site and Content. BROKSTOCK SA (PTY) LTD is not liable for any direct, indirect, incidental, consequential, special or punitive damages. Working with BROKSTOCK SA (PTY) LTD you are trading share CFDs. When trading CFDs on shares you do not own the underlying asset. Share CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. A high percentage of retail traders accounts lose money when trading CFDs with their provider. All rights reserved. Any use of Site materials without permission is prohibited.